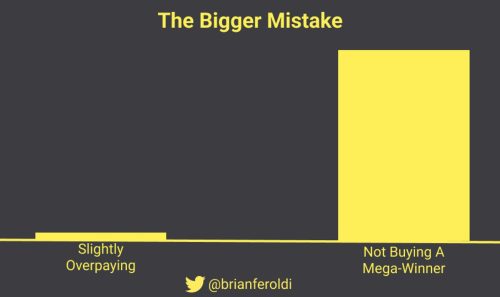

🧠 Are We Overpaying?

Friends,

Which of these two stocks would you invest in?

Stock #1

- Expenses have increased 260% since 2019.

- Gross margins have contracted over that time.

- The P/E ratio is over 200.

Stock #2

- Revenue is up 320% since 2019.

- Operating margins have expanded 1,400 basis points over that time.

- The P/FCF ratio is 35.

We hope the answer is obvious.

Stock #2 would definitely win our money. Torrid revenue growth means people love what’s offered. Expanding operating margins suggests there’s a moat present and operating leverage is kicking in. And the valuation — while not cheap — looks reasonable given the top-line growth.

And this isn’t just hypothetical: stock #2 is MercadoLibre. It’s currently a top holding for Feroldi, Stoffel, and Withers (mostly because the stock is up 1,200+% over the last decade.)

But — as you might have guessed — there’s a catch.

Stock #1 is also MercadoLibre.

Why do the numbers look so different? A few reasons:

- Expenses are up because MercadoEnvios (think: Fulfillment by Amazon) costs a lot to build out.

- Gross margins have contracted because MercadoPago (think: PayPal) is based on high volumes — not high margins.

- The P/E ratio currently looks “insane” mostly because of the accounting differences between earnings and free cash flow.

We know how confusing that last point can be. Valuation can be incredibly tricky subject. When we released a video on your YouTube channel saying we’re adding to our MercadoLibre position in our model portfolio, several commenters said we were “crazy” to buy in a stock with a P/E ratio over 200.

Only time will tell if we are overpaying, but we think there are two key takeaways to remember:

- Context matters: We know this to be true in our non-investing lives, but often forget it when it comes to investing.

- Valuation is part art & part science: if you choose to invest in individual stocks, you need to understand which valuation metrics matter, when they matter, and when they should be ignored.

We’ve made plenty of investing & valuation mistakes ourselves. Our hope is that by sharing our blunders publicly, our readers will avoid making many of the mistakes that we already have.

That’s the wonderful thing about investing. It’s an activity where we can help each other do better.

We’re glad to be on that journey with you.

– Brian Feroldi, Brian Stoffel & Brian Withers

P.S. If valuation is a topics that interests you, join us next Tuesday, February 21st at 12:00 EST. We’re hosting a free webinar that answers one of the most basic valuation questions: Why do stocks have value?

In Partnership with ConvertKit

Newsletter Sponsorships Work

Guess what? You’re reading promotional content in a newsletter. Sponsoring influencer newsletters, like this one, is a great way to reach engaged and targeted audiences. It will build your brand — whether that is your personal brand or your business.

So here is the deal. This newsletter is part of the ConvertKit Sponsor Network (CKSN), representing more than 100 individual newsletter creators. Sponsor my newsletter and gain access to many more.

Sponsors Long-Term Mindset Now

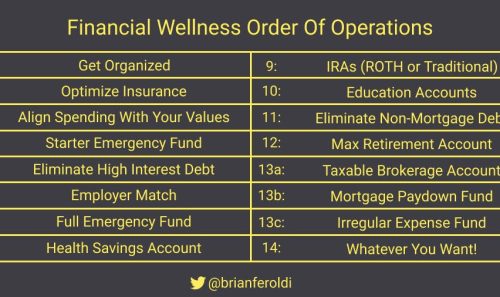

One Simple Graphic:

|

|

One Piece of Timeless Content:

Lawrence Yeo introduces his blog by saying: “Life as a human is a weird experience, but one that I’m grateful to be a part of. And when you have a sense of gratitude for the peculiar, you get a little something called curiosity.”

His post, The Nothingness of Money, provides a powerful life lesson on how we think about money.

One Twitter Thread:

Checking your portfolio results frequently could be making you miserable. This wonderful thread by 10-K Diver (one of our favorite follows on Twitter) breaks down this concept beautifully:

December 11th 2022

|

One Resource:

Kurtis Hanni worked as a small business CFO for more than 15 years helping owners understand their financial statements and make strategic decisions. His newsletter Frameworks & Finance shares one lesson each week to help you speak “the language of business.”

One Quote:

|

|

More From Us:

👨🎓 NEW! You asked, we answered. The #1 request we get from students is a course that demystifies valuation. Called Valuation Explained Simply, this new cohort-based course launches on March 14th. Join the waitlist.

📗 Brian Feroldi’s book is on sale.

.png)