🧠 We Made A Mistake

|

View Online | Sign Up | Advertise Welcome to Long-Term Mindset, the Wednesday newsletter that helps you invest better. Today’s Issue Read Time: <3 minutes

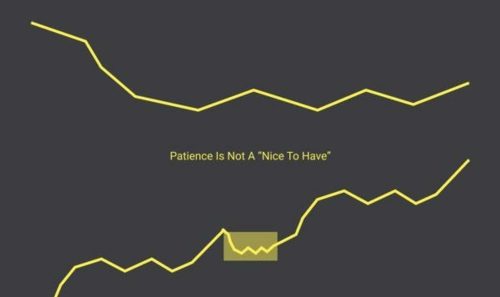

Friends, If you’ve followed us for any period of time, you’ve likely seen us share this fantastic graph:

We’ve used it constantly to emphasize that valuation (multiple) is not the end-all, be-all of investing. It shows that revenue and profit growth are far more important. But we’ve highlighted a part that’s often ignored (including by us):

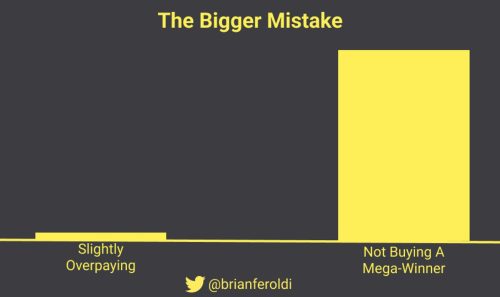

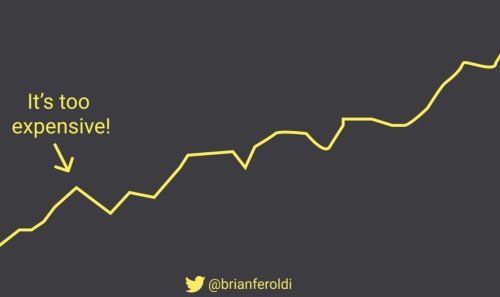

Let’s think about this for a minute. By selecting the top quartile of stocks for returns, we’re already throwing out 75% of the S&P 500. That shouldn’t be overlooked — and yet we’ve consistently overlooked it! Why does this matter? Well, let’s look at three of the best-performing stocks between 2010 and 2020:

All three companies share something in common: they grew revenue ridiculously fast. Netflix transitioned to streaming, DexCom eliminated the need for diabetes patients to draw blood, and TransDigm became the one-stop shop for the airline industry. Importantly, all three grew far faster than even the most bullish analyst was predicting in 2010. There are two reasons this caveat matters:

Think about it: If I pick an “expensive” stock that returns 5,000% over the next decade, I can crow that valuation doesn’t matter. If I pick that same stock and it tanks, it won’t be included in this data set. None of this is to say we’ve done a 180 on valuation. We still believe a company’s moat, optionality, financial fortitude, and culture are the primary drivers of future returns. But we’ve realized — painfully — that you can’t ignore valuation either. And valuation is probably the trickiest part of investing. There’s no one-size-fits-all approach. It largely depends on what type of investor (and person) you are. If you want to level up your valuation skills, join us for a free webinar on April 11th (tomorrow) at noon EDT. We’ll show you how super investors like Warren Buffett, Marc Andreesen, and Sam Zell value businesses — and what makes the most sense for you. Click here to register instantly. We hope to see you there – Brian Feroldi, Brian Stoffel, & Brian Withers One Simple Graphic:

One Piece of Timeless Content: Morgan Housel’s focus on the long-term is inspiring. His 2016 interview on Patrick O’Shaughnessy’s podcast, Invest Like The Best, was a great listen and is still relevant today. Topics include the differences between private and public market investing, how businesses are structured, and how Morgan finds topics to write about. One Thread:

One Resource: “Earnings season” is right around the corner. Want to know which companies are reporting this week or next? Finchat’s earnings calendar is a great resource. Simply select a time frame or pick a company of interest. Sort by market cap (largest on top) to find the most popular companies. Best of all, it’s free! One Quote:

👋 What did you think of today’s newsletter? More From Us: 📗 If you’ve read Brian Feroldi’s book, he’d love a review. 👨🎓 The next cohort of our Valuation Explained Simply course starts in May! Click here for details. 🎬 Want a review of popular company earnings? Check out our YouTube channel! Earnings season starts soon; we can’t wait! |