🧠 Why Meta Plunged & Tesla Surged

|

View Online | Sign Up | Advertise Welcome to Long-Term Mindset, the Wednesday newsletter that helps you invest better. Today’s Issue Read Time: <3 minutes

Friends, Last week was a bewildering one for individual investors.

The stock market isn’t broken. Investors often forget something at their own peril: the stock market is a forward-looking entity. Results over the last 90 days only matter so much as it informs what could be coming in the next 90 days (or, in our case, the coming decades). If you dig a little, it actually makes a lot of sense. We ran a reverse discounted cash flow (rDCF) on both companies before earnings were released. What we found was interesting. If we assumed Tesla could achieve 20% free cash flow margins by 2034 (boosted by non-auto sales), then it only needed to grow revenue by 10% to justify its price. When Elon Musk revealed the company is not only working on a robotaxi, but also a low-priced car (the opposite of what news outlets were saying), and the possibility of humanoid robots sales by next year — that 10% revenue growth seemed like a very low hurdle. On the other hand, if we assumed Meta could maintain its 33% free cash flow margins indefinitely, it needed to grow revenue by 13% for the coming decade. The problem arose when Mark Zuckerberg said Meta was beginning a multi-year ramp in AI spending that would require a lot of capital expenditures. Such expenses pull down free cash flow, making that 33% figure seem too high of an assumption. Of course, if you’re a longer-term investor, you should applaud both of these moves. They represent both companies using all of their cash to continue innovating and creating products that further their missions. In the long run, we have little doubt that shareholders will be rewarded when management teams think in decades, not quarters. – Brian Feroldi, Brian Stoffel, & Brian Withers P.S. 👨🎓 The next cohort of our Valuation Explained Simply course starts on May 6th! Click here to enroll with a $149 “Last Call” discount. One Simple Graphic:

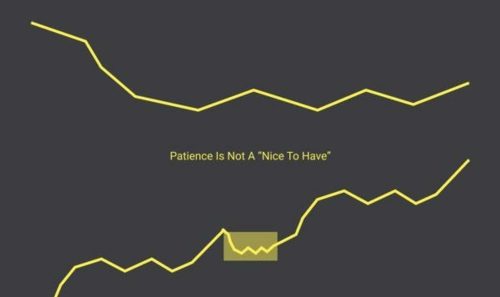

One Piece of Timeless Content: Investing is one of the only pursuits in which doing nothing gets you ahead. In fact, activity bias, or our desire to “do something,” can actually harm our portfolio returns. Want to be a better investor? Check out this article from Tim Hanson titled Just Don’t Do It. One Thread:

One Resource: Chris Hutchins — host of the popular All the Hacks podcast– had Brian Feroldi on as a guest to discuss the benefits of using an investing checklist. One Quote:

👋 What did you think of today’s newsletter? More From Us: 📗 If you’ve read Brian Feroldi’s book, he’d love a review. 👨🎓 The next cohort of our Valuation Explained Simply course starts in May! Click here for details. 🎬 Want a review of popular company earnings? Check out our YouTube channel! Meta and Google earnings videos are now available! |