Cash Flow Statement Explained Simply

The Cash Flow Statement is one of the three financial statements investors must understand to analyze businesses.

The purpose of the cash flow statement statement is to track cash movement. It shows how cash moves through a company over a period of time, such as a quarter or year.

A company’s cash flow statement can be compared to your personal checking account. It doesn’t care about transactions of goods and services being sold or when sales contracts are signed. It only tracks when money is deposited or withdrawn from a company’s bank accounts.

Unlike the income statement and balance sheet, the cash flow statements use cash accounting, not accrual accounting.

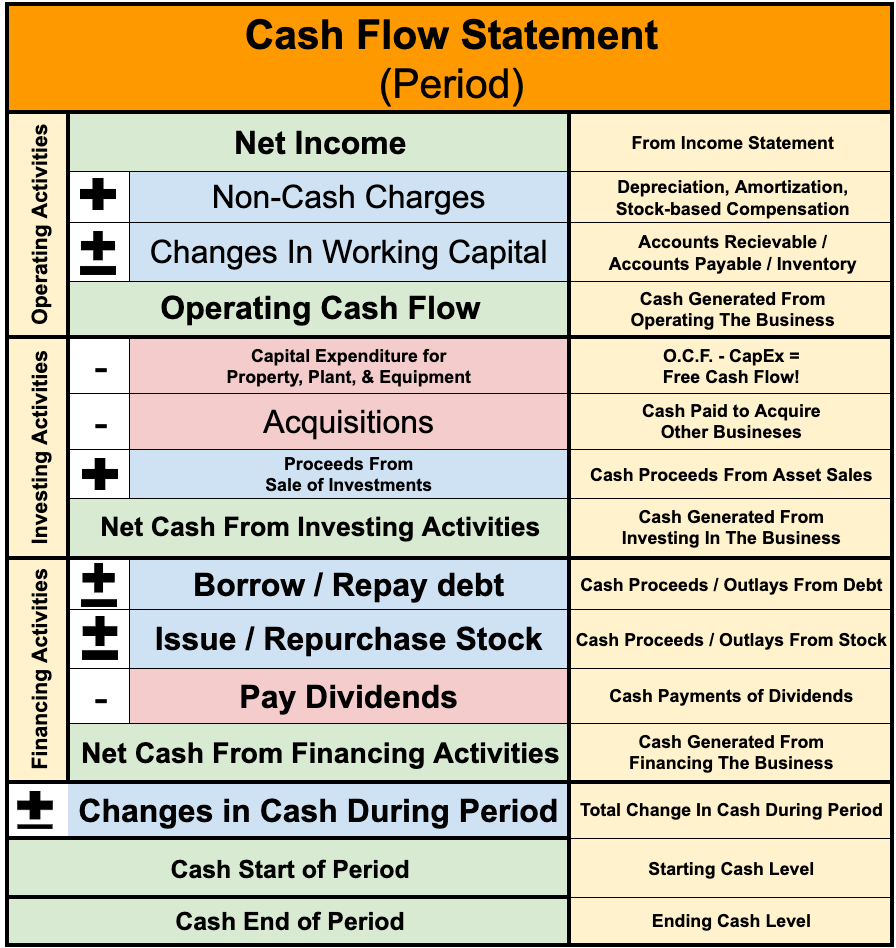

Here is the layout of a typical cash flow statement:

As you can see, the statement is divided into three primary categories:

- Operating activities

- Investing activities

- Financing activities

Continuing with our personal finance comparisons, operating activities are equivalent to the money you need to run your household. This section begins with the net income, then non-cash charges are added back. These charges were accounted for on the income statement but where no cash exchanged hands.

This commonly includes four things:

1) Asset impairment – When the market value of an asset is less than previously stated, such as a company admitting it paid too much for an acquisition.

2) Amortization – The gradual writing off of an intangible asset, much like how yo pay more interest at the start of a mortgage.

3) Depreciation – The gradual writing off of a tangible asset, such as the value of your car decreasing over time.

4) Stock-based compensation – Compensating employees with stock instead of cash.

All of these charges are accounted for on the income statement (though they are not always broken out), but none of them actually involve cash leaving a company’s bank account.

Changes in working capital are the difference between current assets and current liabilities (both from the balance sheet). This can include things such as accounts receivable (e.g. when someone pays for a good or service using credit), inventory that has yet to be sold, or prepaid expenses.

Investing activities are funds used to invest back in the business, either for growth or to maintain assets. This is cash used beyond the scope of a company’s daily operations, such as building a new factory or acquiring another business.

It’s similar to remodeling your kitchen or painting your house. That’s not running your household; that’s maintaining and investing in your home.

Financing activities are how cash flows in and out based on financial activity. For public companies, this includes issuing bonds or new stock (producing positive cash flow) or paying dividends and buying back shares (generating negative cash flow).

Investors should focus on two key metrics from the cash flow statement: operating cash flow and free cash flow.

Operating cash flow is the cash generated from normal business operations, almost equivalent to net income from the income statement on a cash basis.

Free cash flow is one of the most essential numbers a business generates, but it isn’t always shown on the cash flow statement.

Free cash flow results from subtracting capital expenditures (CapEx) from operating cash flow. CapEx are funds a company uses to build new or maintain existing physical assets, such as factories, equipment, and machinery.

Lastly, the bottom section of the cash flow statement shows the cash the company started with at the beginning of the quarter or year and compares it with the money it ended the period with.

The cash the company ends with is also shown on top of the balance sheet’s assets section in the cash and cash equivalents line.

So, the cash flow statement begins with the end of the income statement and ends with the beginning of the balance sheet. This is how all three financial statements connect to show a complete 360 view of a company’s financial performance.

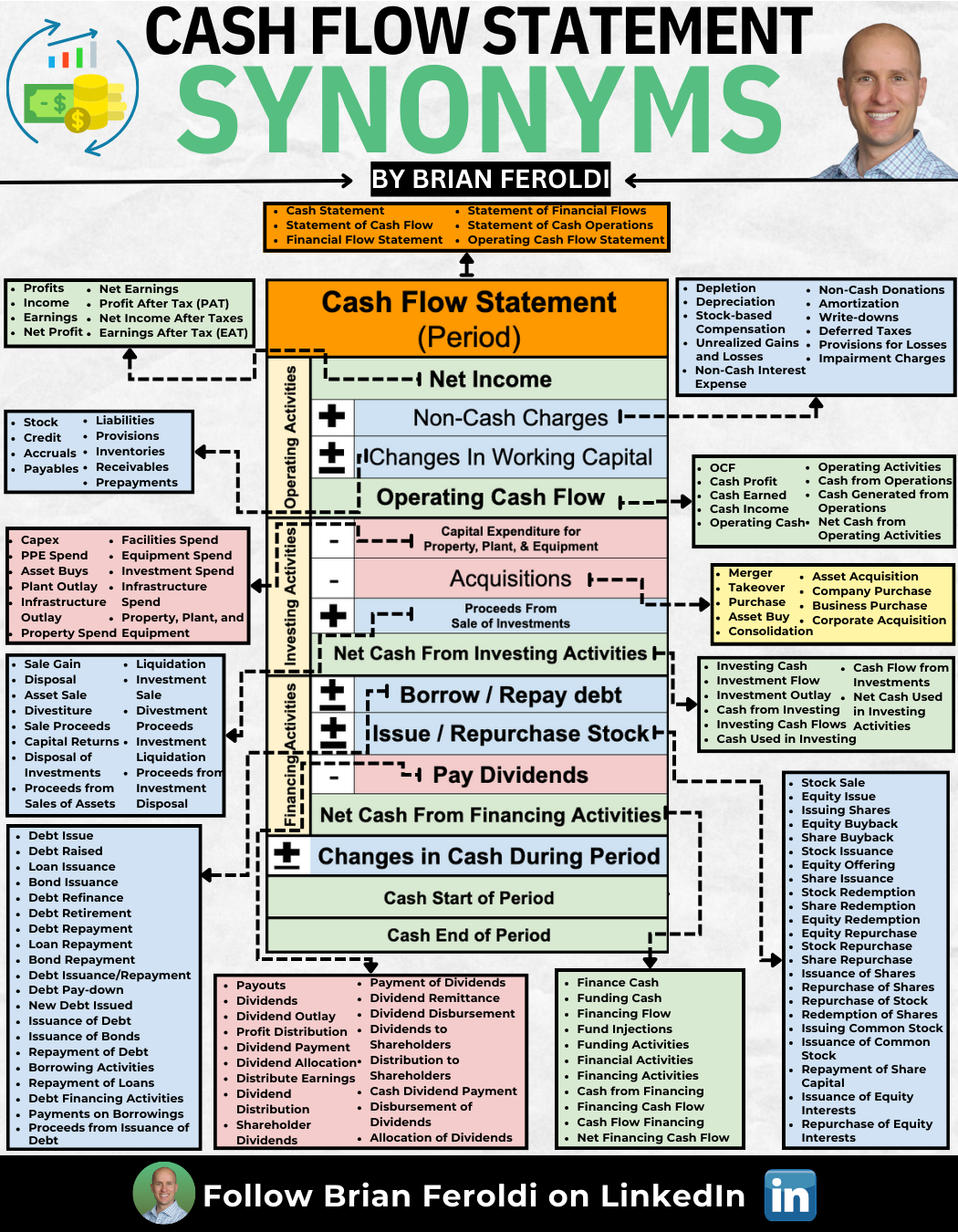

It’s worth noting that management teams have complete control over the layout of their cash flow statement and the terms they use. Here are some other terms you may see used on a cash flow statement:

So why do investors say that “cash is king”?

Many companies can appear profitable on their income statements despite never generating positive free cash flow.

Positive free cash flow gives companies vital flexibility, allowing them to invest for growth, make long-term strategic moves, and reward shareholders.

Understanding these key terms and how each was reached will help you become a better investor.